•

5 Mins Read

Key Summary:

Enron's collapse wiped out $74 billion in shareholder value and destroyed one of the world's largest accounting firms. But the article argues that fraud wasn't the most important lesson hidden inside the scandal.

Fortune named Enron "America's Most Innovative Company" six consecutive times, and its board was packed with experts. The question is: how did so many smart people miss what was happening?

Warning signs existed years before the bankruptcy, yet complexity and success made skepticism increasingly uncomfortable. The article explores why admiration can sometimes become more dangerous than incompetence.

From Enron to Kodak, Nokia, and Blockbuster, history reveals the same pattern. Organizations often fail not when people stop believing, but when too many people believe the same story for too long.

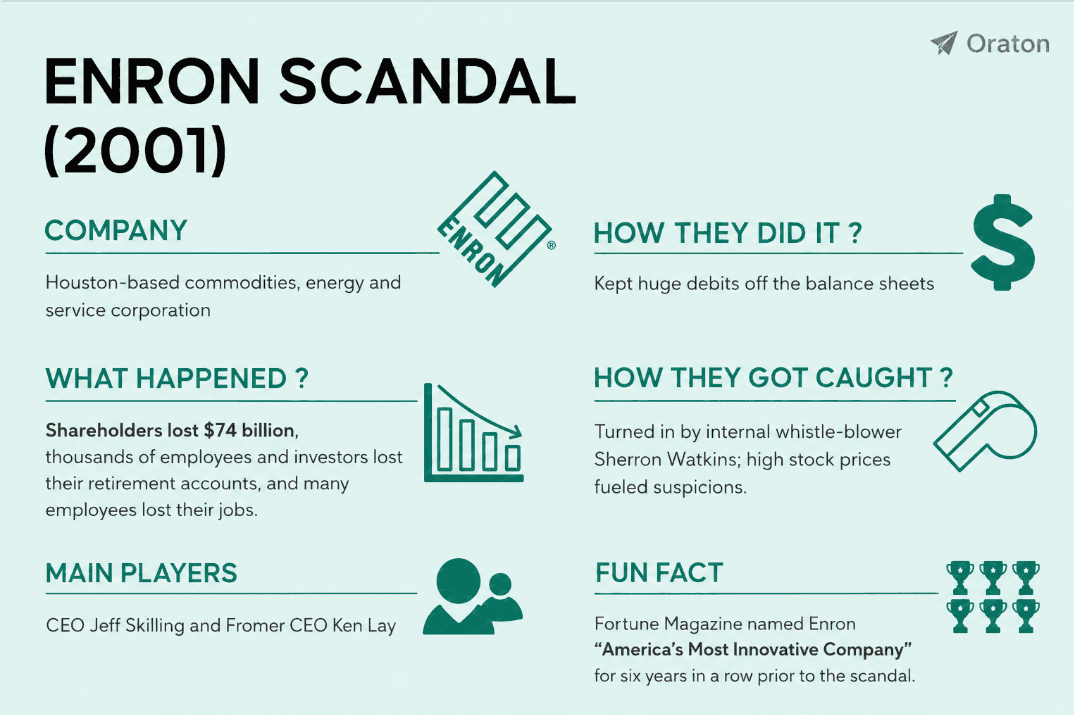

When Enron filed for bankruptcy on December 2, 2001, it represented the largest corporate collapse in American history. The company had amassed $63.4 billion in assets, employed more than 20,000 people, and destroyed approximately $74 billion in shareholder value. Thousands of employees lost not only their jobs but also much of their retirement savings, while Arthur Andersen, one of the five largest accounting firms in the world, effectively ceased to exist after its role in the scandal came under scrutiny. More than two decades later, Enron remains synonymous with the corporate fraud term. Yet reducing the story to greed, accounting manipulation, and executive misconduct risks overlooking the deeper story hidden beneath one of the most studied failures in business history.

The uncomfortable truth is that Enron did not collapse because a few individuals managed to fool everyone else. It collapsed because an entire ecosystem gradually lost the ability, and perhaps the willingness, to challenge success itself. Investors were enthusiastic. Analysts were impressed. Journalists celebrated the company. Fortune magazine named Enron "America's Most Innovative Company" six years in a row between 1996 and 2001. The board was filled with accomplished outsiders. Its audit committee included accounting experts, former government officials, and experienced executives. On paper, Enron looked exactly like the kind of company modern governance frameworks are designed to produce.

This is what makes the story so fascinating from a leadership perspective. Enron did not fail in spite of intelligence, it rather failed alongside intelligence. It did not lack expertise, it was overflowing with big names from the industry and outside. The company recruited some of the brightest people in the country. Jeffrey Skilling's reputation was legendary. Analysts admired the sophistication of Enron's financial models. Wall Street celebrated its relentless growth and everyone seemed to agree that they were looking at one of the most innovative organizations in America.

And that consensus turned out to be precisely the problem.

Most people imagine governance failures beginning with incompetence. In reality, many begin with admiration. Once an organization becomes associated with success, questioning it starts to feel irrational. Skepticism begins to resemble negativity. Dissent starts to look like ignorance. Eventually, people stop asking difficult questions not because they are incapable of doing so, but because the surrounding narrative makes those questions increasingly uncomfortable.

This dynamic appears repeatedly in organizations. A star CEO delivers several successful quarters, and suddenly their assumptions receive less scrutiny. A high-performing division generates exceptional returns, and unusual metrics stop attracting attention. A founder becomes synonymous with the company's identity, and criticism begins to feel almost disloyal. Performance creates credibility. Credibility creates trust. And trust, left unchecked, can slowly erode the very skepticism that healthy institutions depend upon.

Enron's internal culture amplified these tendencies. Compensation systems became heavily tied to stock price, encouraging employees and executives to focus obsessively on short-term earnings. Between 1998 and 2000, compensation for the company's top 200 employees exploded from $193 million to $1.4 billion. Executives were rewarded for generating deals and maintaining growth expectations, often with little regard for the underlying quality of those earnings. In such an environment, success itself became the metric. Nobody wanted to be the person asking whether the emperor had clothes when the stock price kept rising.

Perhaps the most remarkable aspect of Enron's collapse is that warning signs existed long before the bankruptcy. Analysts raised concerns. Internal whistleblower Sherron Watkins questioned accounting practices. Certain transactions appeared unnecessarily complex. But complexity itself became a shield. The more difficult the business became to understand, the easier it became for people to assume that the smartest people in the room must know something they didn't. Complexity discouraged scrutiny. Sophistication created deference.

Boards face this challenge constantly. Directors often assume their greatest responsibility is approving strategies and monitoring performance. Yet history suggests their most important responsibility may be something far less glamorous: preserving the organization's capacity for doubt. Healthy governance is not simply about oversight, it is about maintaining enough intellectual independence to ask uncomfortable questions, especially when success makes those questions feel unnecessary.

Ironically, Enron's board looked impressive by conventional standards. Its members possessed expertise. Its audit committee was stronger than many of its peers. Meetings were held. Reports were reviewed. Procedures existed. Yet a Senate investigation later concluded that conflicts of interest, information asymmetries, and a lack of understanding surrounding complex financial structures prevented the board from exercising effective oversight. The mechanisms of governance were present. The mindset of governance was not. This distinction matters because governance is ultimately less about structure and more about psychology. Companies can create committees, policies, and controls, but none of those mechanisms matter if the people inside the system become emotionally invested in a particular narrative. And few narratives are more intoxicating than success. Success creates confidence. Confidence creates certainty. Certainty reduces curiosity. And when curiosity disappears, organizations become extraordinarily vulnerable. The same pattern explains why companies such as Kodak struggled with digital photography, why Nokia underestimated smartphones, and why Blockbuster dismissed streaming. Their failures did not originate from ignorance. They originated from confidence built on past victories. Yesterday's strengths became tomorrow's blind spots.

This is perhaps the deepest lesson hidden inside Enron's story. Leaders often worry about skepticism undermining morale, slowing decisions, or creating unnecessary friction. Yet some degree of constructive skepticism is precisely what protects organizations from their own narratives. The strongest boards are not the ones that eliminate disagreement. They are the ones that institutionalize it. The strongest cultures are not those where everyone agrees. They are those where questioning remains socially acceptable, even when results are strong.

Because success creates a strange paradox. The better things appear to be going, the more dangerous it becomes to assume they will continue and that may be the most enduring lesson from Enron.

Companies rarely collapse because people stop believing. They collapse because too many people believe the same thing for too long, without much questions.

Previous

Spain dominated every statistic, but Cape Verde left with the momentum. The match offers a surprising lesson about leadership, expectations, and why narratives often shape performance more than talent.

Next

The most watched presidential debate in modern history revealed an uncomfortable truth about influence. 8 years later, its biggest lesson may have less to do with politics and more to do with how leaders create clarity.